Dr. Richard Michaud and son, Robert Michaud, are co-CEOs of the innovative financial firm New Frontier Advisors. New Frontier is a Boston-based institutional research and investment advisory firm specialising in the development and application of state-of-the-art investment technology.

Richard “Dick” Michaud pairs his academic background with years of practitioner experience. He passionately advocates for improvements in financial practice across the industry. Robert, the CIO, oversees the investment process and technology. Both Dick and Robert are heavily involved in research, striving to consistently improve New Frontier’s investment process and provide value to investors.

You are known as a research, technology and investment company. This is quite unusual for a finance company. How do the three sides of your business work together?

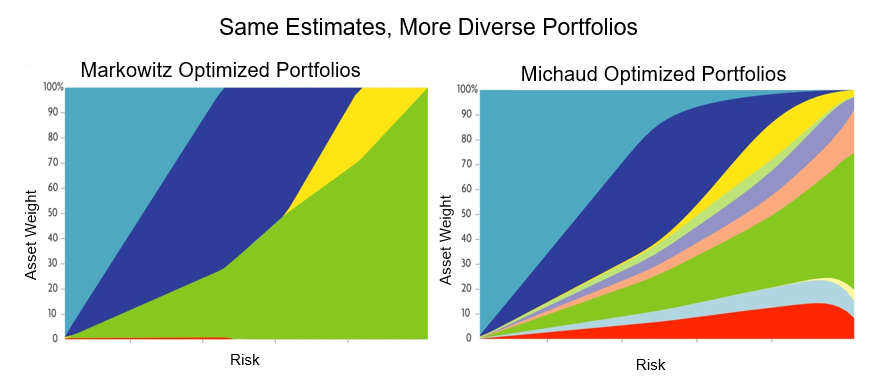

Richard: Research is the foundation of everything we do. We started the company based on our research for mathematically optimising portfolios when the future risk and return of the assets you want to invest in isn’t precisely known. This was a happy example of research with practical implications. The early years of the company were spent building out a full suite of investment technology. This allowed us to build a range of portfolio strategies for different investor objectives using a consistent investment process based on our research and implemented with only our technology. We keep working in all three areas through a positive feedback system of research, technology and investments to improve upon everything we do. It seems to have worked — every portfolio strategy we’ve ever launched has continued to grow and is still being used today.

Another thing that’s unusual about us is that we were able to patent some of the key ideas and publish books and research papers for many of the others. In stark contrast to black box investment strategies and “proprietary research” common in other finance companies, there’s a tremendous amount of transparency in our technology and investment products. In finance, where risk comes from many sources, transparency can lead to a high level of comfort for our clients.

Your recently introduced index, NFGBI, is an interesting offshoot of your ideas. Can you explain what’s special about this index?

Robert: I’ve always had a love/hate relationship with indices. They give a precise summary of market information, but it’s never been clear why they’re relevant or which index I should focus on. When following a combination of stock, bond, commodity, interest rate and international indices, it’s not always clear if they represent good news or bad, especially when some are up and others are down. What’s lacking is a complete measure of whether we’re better off or not. That’s why I’m excited about NFGBI. It summarises 27 global asset classes optimally weighted to suit a typical investor holding a 60/40 portfolio. The asset classes cover stocks, bonds, domestic, international and emerging markets, large and small companies, real estate, gold and more. For most investors, it’s the only index they should follow.

The failure of active strategies to outperform their benchmarks has attracted many investors to passive strategies. Is the active management industry in crisis?

Robert: It shouldn’t be surprising that active strategies underperform. The simple math of the market shows that after fees the average investor can’t outperform the market. Active management will always have the critical role of valuing assets and keeping markets efficient, but not all investors need to invest in active funds for that to happen. My father’s latest research on Finance’s Wrong Turn is a deeply insightful explanation of why too much of the investment industry fruitlessly tried to beat the market. There’s a lot to say about this, but it has become clear that most investors are better served by designing portfolios to meet investment goals rather than hoping for excess returns from active managers.

New Frontier has portfolios with a 13-year track record as one of the earliest successful ETF strategists. Please explain the firm’s investment philosophy and methodology.

Richard: Early on in the development of the firm, given our increasing reputation in state-of-the-art investment technology, we were invited to become ETF strategists. As a consequence we were one of the first to manage a portfolio of global ETFs. We invest in global economic growth for long-term investors. Our focus is on controlling risk rather than short term market forecasts. During the downturn in 2008 we held to our long-term view and our faith in our technology as providing effective portfolio diversification and quality risk management. It’s been gratifying to see our performance on places like Morningstar, where we are consistently ranked highly.

We offer tax-deferred, tax-managed, and income portfolios across the global systematic risk spectrum. We create all of them from the ground up with that objective in mind. For instance, our taxable portfolios don’t simply replace taxable bonds with municipal bonds as many managers do. Instead, Michaud optimisation creates portfolios where every allocation is precisely calculated to maximise after-tax risk-adjusted return.

In addition to using Michaud optimisation to create the portfolios, we use Michaud-Esch rebalancing to maintain them. Rather than trading on a calendar basis or when portfolios cross certain weight ranges, we test every day to see if the currently held portfolio differs significantly from the most up to date optimal portfolio and only trade when it’s likely to benefit the investor. We avoid costly trading in statistical noise and reduce unnecessary taxes and trading costs for investors.

New Frontier is interesting in that it is a father-son team that drives investment decisions. You’ve written research papers, a book, and even share four patents in portfolio optimisation and asset management. How did that partnership evolve?

Richard: One of my greatest joys in life has to do with my relationship with my son. We have always enjoyed bouncing ideas off each other even when he was very young. Robert was always gifted, one could even say a computer technology prodigy. He loved to compete with his gifted computer friends on who could produce the most compact efficient code for any kind of game or problem. His facility at implementing scientific ideas was a great asset as we began our research together. His first most notable collaboration was on the first edition of the book, Efficient Asset Management, where we jointly came up with the idea of improving Markowitz’s Nobel Prize winning work to account for estimation error uncertainty in investment information. I decided to start a company on this major new idea. Robert was excited too—he entered a finance Ph.D. programme and later built the company with me. From that patent, we started our business creating investment technology and offering consulting. Then in 2004, AssetMark asked us to start offering ETF portfolios, so we entered investment management. Every portfolio strategy we’ve launched has thrived to this day, but ideas remain central to what we do. We continue to motivate each other to keep up with the latest research in mathematics, computer technology, mathematical statistics, and financial theory and practice to improve our investment process.

What is next for you and New Frontier?

Richard: My interest is to continue to work with my son and my esteemed colleagues at New Frontier to innovate in investment technology and asset management. There is much to do. Global investing has become the norm. The challenges of correctly understanding a wide range of economic cultures and markets, implications of regulations, and susceptibility to geopolitical influences are very exciting. And, as my recent course suggests, finance in practice is in a serious reboot mode. New tools that are very different from those from the 20th century need to be invented. New opportunities and innovations are all part of the challenges and opportunities for building a new kind of asset management firm providing more reliable investment strategies that meet the relevant investment horizons of investors and institutions.

Disclosures: Past performance does not guarantee future results. Diversification may not protect against market risk. There are risks involved with investing, including possible loss of principal. Before investing in any investment portfolio, an investor should consult with a financial advisor and carefully consider investment objectives, time horizon, risk tolerance, and fees.

Website: https://www.newfrontieradvisors.com/